Polkadot 2.1B DOT Supply Cap Changes the Validator Economics Conversation

Overview

July 7, 2026. Polkadot's 2.1B DOT cap is no longer just a governance headline. It is now an operating assumption for validators, delegators, treasury voters, and anyone trying to understand the network's long-term economics.

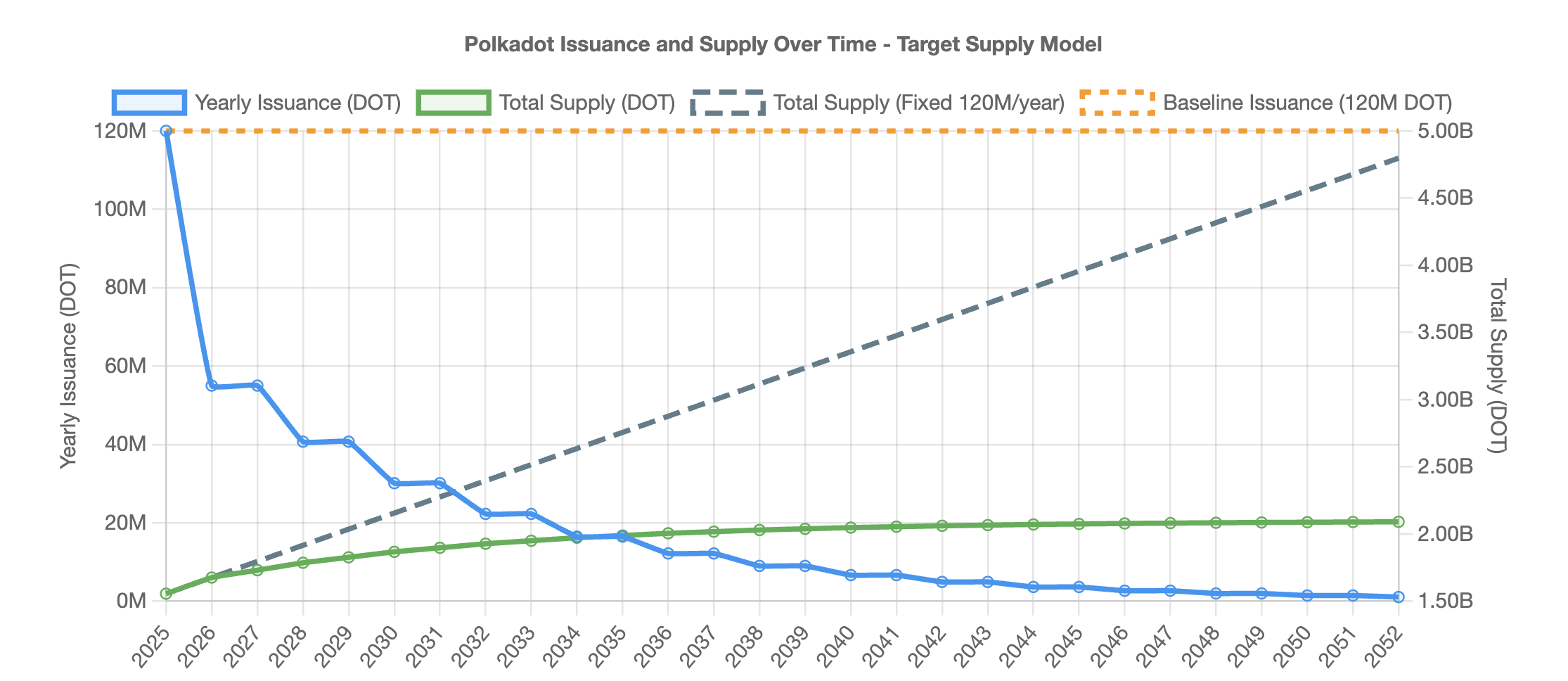

Referendum 1710 changed the shape of DOT issuance. Instead of an open-ended inflation path, Polkadot now has a maximum supply target of 2.1B DOT and a stepped schedule that mints 13.14% of the remaining unissued supply every two years, beginning from the March 14, 2026 activation point.

Context

That sounds like tokenomics language, but the practical impact is simpler: staking yield now has to be read with more discipline. A headline APR does not say enough on its own. The better question is whether the reward is still attractive after dilution, validator commission, treasury spending, and actual network demand are all taken into account.

The Cap Changes the Baseline

The old model made DOT rewards easier to describe but harder to value. If issuance can continue indefinitely, nominal staking rewards can look healthy even while long-term dilution remains an open question.

Operational Impact

The new model puts a ceiling over that conversation. Issuance still exists, validators still earn rewards, and delegators still have incentives to stake. But the network is no longer leaning on unlimited expansion of supply as the background assumption.

That matters for every audience.

Operator Actions

For delegators, the question becomes: am I earning a real return, or just receiving more units from a system that is diluting everyone else?

For validators, the question becomes: can I attract and retain stake because my operation is reliable, fairly priced, and useful to the network?

Risk Watch

For governance voters, the question becomes: does treasury spending create enough network value to justify capital leaving a now-constrained monetary base?

The supply curve is the visual point. Polkadot has not eliminated issuance; it has made issuance more predictable and progressively constrained. That changes how rewards should be interpreted.

Delegators Need to Think in Real Yield

A delegator looking only at staking APR is now missing half the picture.

The useful questions are more specific:

- How much of the return survives after issuance and dilution are considered?

- Is the validator commission fair relative to performance and reliability?

- Does the validator contribute to decentralization, governance quality, or network resilience?

- Is the network producing enough demand to make constrained supply matter?

This is not a call to ignore APR. Rewards still matter. But a capped supply model makes lazy APR comparison weaker. A validator with slightly lower nominal yield but stronger uptime, better governance behavior, and a more sustainable commission policy may be the better long-term choice.

That is the audience shift: staking becomes less about chasing the biggest displayed percentage and more about selecting durable economic participation.

Validators Face a Sharper Market

Validators should read Referendum 1710 as a change in their operating environment.

In an uncapped inflation model, high issuance can smooth over weak economics for longer. Under a declining issuance path, validator quality becomes more visible. Commission policy, uptime, governance participation, infrastructure discipline, and stake attraction all matter more because rewards sit inside a more constrained monetary envelope.

That does not make validation less attractive. It makes validator economics more competitive.

The strongest operators will be the ones that can explain their value clearly: reliable performance, sensible fees, transparent operations, and a reason for delegators to stay when nominal reward rates evolve.

The Treasury Also Gets a New Constraint

This change is not only about staking.

A hard cap changes how treasury spending feels. When supply is open-ended, future issuance can blur the cost of ecosystem funding. When supply is capped, capital allocation becomes easier to scrutinize.

That does not mean the treasury should stop spending. It means spending needs to be tied more visibly to outcomes: more useful applications, stronger coretime demand, better developer retention, better liquidity, better infrastructure, and more reasons for users to hold or use DOT.

The cap raises the standard for treasury strategy. That is healthy if governance responds with discipline.

Scarcity Is Not Demand

The most important caveat is this: a cap does not automatically create value.

It improves the monetary foundation. It makes dilution more predictable. It gives investors and analysts a cleaner model. But scarcity only matters when the asset sits inside a system people want to use, secure, build on, or allocate around.

That is where Polkadot's next phase becomes more interesting. The supply side is now clearer. The demand side has to keep proving itself through coretime usage, application growth, ecosystem revenue, and credible governance execution.

Referendum 1710 does not finish the economic story. It makes the story measurable.

How to Read Polkadot From Here

The useful indicators are no longer only issuance and staking APR.

Watch the full stack:

- staking participation and validator commission trends

- treasury spend quality and measurable ecosystem outcomes

- coretime demand and infrastructure usage

- validator concentration and delegation behavior

- whether DOT demand grows alongside the constrained supply path

That is the real economic conversation now. Polkadot has put a hard ceiling on supply. The next test is whether the network can make the capped asset more productive.

Sources

- Polkadot now has a 2.1B DOT maximum supply under Referendum 1710.

- Issuance follows a two-year step schedule based on 13.14% of remaining unissued supply.

- Delegators should judge staking by real yield, commission quality, and network productivity.

- Validators now compete in a constrained model where reliability and stake attraction matter more.